I still remember the moment I held the keys to my first home. It wasn't just metal in my hand; it was a mix of overwhelming pride and sheer exhaustion. Let's be real—buying a home in the U.S. is likely the biggest financial decision you'll ever make, and the process can feel like navigating a maze blindfolded. Between fluctuating interest rates, tight inventory, and confusing paperwork, it's easy to feel lost.

But here is the good news: you don't have to learn everything the hard way like I did. While the market may be complex, a clear strategy can save you thousands of dollars and countless sleepless nights. I've compiled the 10 most essential tips that served as my roadmap—steps that transform the chaos of buying into a smart, calculated investment.

Financial Foundations: Get Your Money in Order First

Before you even look at a "For Sale" sign, you need to look at your bank account. This is the unglamorous part of home buying, but it is the foundation that holds everything else up.

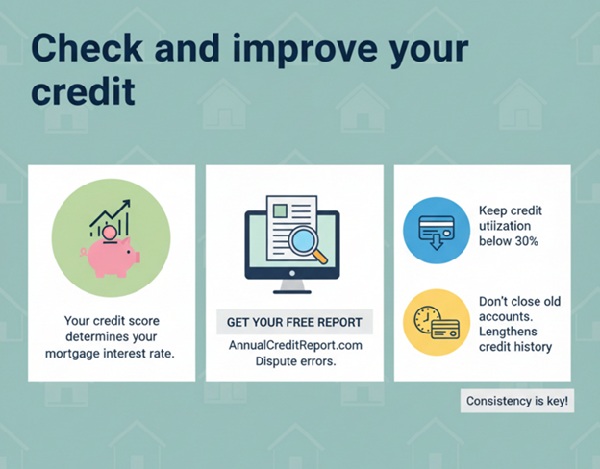

Tip 1: Check Your Credit Score and Boost It Early

Think of your credit score as your financial report card. When I first started, I didn't realize that a difference of just 20 points could change my mortgage rate significantly, costing—or saving—me tens of thousands over the life of the loan.

Most lenders today are looking for a FICO score of 620 or higher for a conventional loan. If you are considering an FHA loan, you might qualify with a score as low as 580 (with a 3.5% down payment). However, to unlock the "VIP" rates, you generally want to aim for 760+.

Go to AnnualCreditReport.com right now. It's free. Check for errors—like a bill you paid that's marked as late—and dispute them immediately. Also, keep your credit cards open but paid down; closing old accounts can actually hurt your score temporarily.

Image: Bluerate

Image: Bluerate

Tip 2: Save for a Substantial Down Payment

There is a stubborn myth out there that you need a 20% down payment to buy a home. Let me bust that right now: You don't. In fact, according to recent data from the National Association of Realtors, the average first-time buyer puts down significantly less, often between 6% and 7%.

• Conventional loans can require as little as 3% down.

• FHA loans typically require 3.5%.

However, there is a trade-off. If you put down less than 20%, you will likely have to pay Private Mortgage Insurance (PMI), which is an extra monthly fee. I suggest aiming for the "sweet spot"—save as much as you can to lower your monthly payment, but don't drain your emergency fund to hit that 20% mark if it leaves you house-poor. Also, don't forget that "gift funds" from family are a legitimate way to boost your down payment, provided they are documented correctly.

Tip 3: Get Pre-Approved for a Mortgage

I learned the hard way that a "Pre-qualification" is just a casual estimate. A Pre-approval, on the other hand, is a power move. It means a lender has actually verified your tax returns, bank statements, and credit, and is willing to lend you a specific amount. In a competitive market, sellers won't even look at your offer without one.

This helps you shop with a real budget, not a guess. But don't just walk into a big bank branch and hope for the best. Finding a specialized loan officer who understands the nuances of your local market can be a game-changer.

For instance, if you are looking in California, you might want to consult Houtan Hormozian. He specializes in helping buyers navigate complex financial situations that big automated banks often reject. You can schedule a free consultation with him to get a clear picture of what you can truly afford before you fall in love with a house.

Smart Shopping: Research and Prioritize Wisely

Once your finances are solid, the fun part begins. But without discipline, "fun" can quickly turn into "overwhelmed."

Tip 4: Define Your Must-Haves vs. Nice-to-Haves

We all want the granite countertops, the three-car garage, and the pool. But unless you have an unlimited budget, you will have to compromise. I recommend sitting down with a partner (or just yourself) and making two distinct lists.

• Must-Haves: These are non-negotiable. Location is usually number one (you can change a kitchen, but you can't move the house). The number of bedrooms and school districts also fall here.

• Nice-to-Haves: This is the stuff that's pretty, like hardwood floors or a finished basement.

Stick to your "Must-Haves" rigidly. If a house has a beautiful kitchen (Nice-to-Have) but adds 45 minutes to your commute (violating a Must-Have), walk away.

Tip 5: Research the Local Market Thoroughly

Don't just rely on the listing price; it's often just a marketing number. I spent hours on sites like Zillow and Redfin looking at "Comps" (comparable sales)—homes similar to the one I wanted that sold recently.

Pay attention to Days on Market (DOM).

• High DOM: If houses are sitting for 60+ days, it's a buyer's market. You have room to negotiate price.

• Low DOM: If houses vanish in 3 days, you need to be ready to move fast and offer strong.

Also, keep an eye on seasonality. I found that shopping in winter often meant less competition, whereas spring is a bloodbath of bidding wars.

Tip 6: Hire a Buyer's Agent

Buying a home without an agent is like going to court without a lawyer—possible, but risky. A good agent is your fiduciary; they are legally bound to look out for your best interests, not the seller's.

Following the 2024 NAR settlement, the rules have changed. You will now likely be required to sign a Buyer Representation Agreement before an agent can even show you a home. This document clarifies how much the agent gets paid. While sellers often cover this cost, it's no longer guaranteed, so this is a crucial conversation to have upfront.

Interview a few agents. Ask them: "How do you help me win in a multiple-offer situation?" Their answer will tell you everything you need to know.

Due Diligence: Inspect and Negotiate Thoroughly

You found "the one." Now, you need to make sure it's not a money pit.

Tip 7: Always Order a Professional Home Inspection

I cannot stress this enough: Never waive the inspection contingency. In a hot market, it's tempting to drop it to make your offer look better, but it is dangerous.

A general home inspection costs a few hundred dollars but can save you thousands. I once walked away from a "perfect" Victorian home because the inspector found active termites and knob-and-tube wiring that would have cost $30k to fix. Use the inspection report as leverage. If the roof is leaking, you don't have to walk away—you can ask the seller to fix it or give you a credit to do it yourself.

Tip 8: Understand All Hidden Costs Beyond the Price Tag

Your mortgage payment is not just the loan repayment. You need to calculate PITI: Principal, Interest, Taxes, and Insurance.

• Property Taxes: These can fluctuate wildly by county.

• Homeowners Insurance: Essential for protecting your asset.

• HOA Fees: If you buy a condo or in a planned community, this fee is mandatory and can rise over time.

Also, budget for Closing Costs. These caught me off guard. They typically run 2% to 5% of the purchase price. So on a $400,000 home, you could need an extra $8,000 to $20,000 in cash on closing day.

Closing and Beyond: Seal the Deal Right

You are at the finish line. Stay sharp—mistakes here are permanent.

Tip 9: Review Every Document Carefully Before Signing

Three days before you close, you will receive a document called the Closing Disclosure (CD). Compare this line-by-line with the Loan Estimate you got at the beginning.

• Did the interest rate change?

• Are the closing costs higher than expected?

• Is there a typo in your name?

Wire fraud is real. If you get an email saying "Wiring instructions have changed," do not click it. Call your title company on a verified phone number to confirm before sending a single cent.

Tip 10: Plan for Move-In and Long-Term Ownership

Congratulations, you own it! But the work isn't done.

• First Move: Change the locks immediately. You don't know who has a spare key from the previous owner.

• Utilities: Set them up a few days before closing so you aren't moving in the dark.

• Emergency Fund: Now that you are the landlord, when the water heater breaks, you have to fix it. I recommend building a "house repair fund" separate from your savings, contributing 1% of the home's value into it annually.

Conclusion

Buying your first home is a marathon, not a sprint. It tests your patience and your finances, but following these steps gives you control over the process.

Let's recap your roadmap:

- 1. Check and boost your credit.

2. Save a smart down payment (doesn't have to be 20%).

3. Get a solid pre-approval.

4. Know your "Must-Haves."

5. Study the market data.

6. Hire a pro agent (and understand their fee).

7. Inspect everything.

8. Budget for hidden costs (PITI + Closing).

9. Review your closing docs like a hawk.

10. Plan for the long haul.

If you are ready to take that first step, don't settle for the first interest rate you see. Transparency is key to saving money. You can use Bluerate to compare personalized mortgage rates and find the best loan officers for your specific needs—completely free. It's the smart way to ensure you aren't overpaying on the biggest loan of your life.